[fancy_header textcolor=”#ffffff” bgcolor = “#9b7095”] ADVERTISEMENT FEATURE [/fancy_header]

Further support for mortgage misfits locked out of borrowing as 1 in 5 expect to be still paying off their mortgage in retirement

Ipswich Building Society has launched its Retirement Mortgage Programme, offering all of its mortgage products to those in retirement as well as to borrowers aged up to 85 years old at the time of their mortgage term ending.

All of the lender’s residential mortgages will accept 100% of a borrower’s pension as well as other forms of income, such as investments, when addressing affordability.

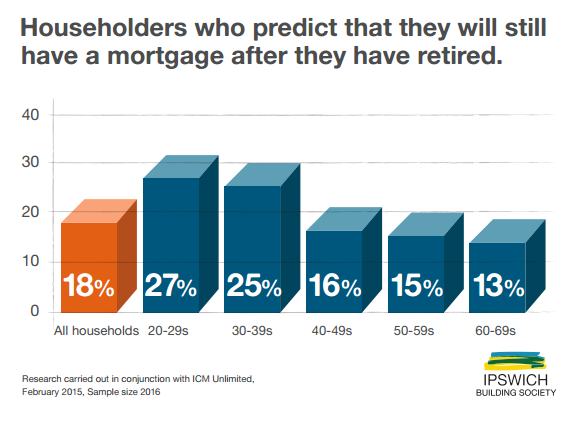

Research among a representative sample of the UK* conducted by Ipswich Building Society has found on average one in five (18%) people expect to be still paying off their mortgage in retirement, including over a fifth (27%) of 20-29 year olds thinking about their future commitments.

A third of the UK overall (33%) are concerned about the availability of mortgage products in the future when they are older, while almost half (45%) believe they will end up paying a higher mortgage rate in the future as a result of their age.

In response to the Mortgage Market Review (MMR) some banks and building societies have restricted lending to borrowers where the term takes them over the age of 65. This has resulted in borrowers in their mid-forties and above having a reduced choice of mortgage providers and products.

Furthermore it limits the life choices of these individuals, for example limiting their ability to release the equity in their property to help family members onto the property ladder or to help address long term health needs.

Commenting on the new programme, Paul Winter, Chief Executive of Ipswich Building Society, said: “Our research has shown the availability of mortgage products is an issue of concern to all age groups, not just those approaching retirement.

Sadly many of the high street lenders have decided to interpret the recent mortgage regulation as a reason to restrict borrowing to older and retired borrowers, adopting a ‘computer says no’ approach to applicants. I don’t believe MMR was ever meant to be used in this way.

Ipswich Building Society is committed to supporting borrowers of all ages as well as those it identifies as mortgage misfits, while retaining a diligent approach to lending.

Examples of mortgage misfits include the self-employed, self-builders, first-time buyers, older generations and those who have experienced a lifestyle change.

Our manual underwriting means we are able to take into account other forms of income, including pensions and investments, more readily.

I would urge my colleagues at other lenders to reassess their product offering and lending criteria for retirees and older borrowers who have been unfairly restricted or alienated from the mortgage market since MMR.”

The mortgage misfits infographic can help borrowers assess if they fall in to any of these groups, and more information about Ipswich Building Society’s Retirement Mortgage Programme can be found at www.ibs.co.uk/olderborrowers.

The new lending programme is available to applicants directly or through a selected group of brokers.

*Research conducted by ICM using online fieldwork during 30 January – 1 February 2015.

Some 2,016 respondents weighted to a representative sample of the UK.

Key features of lending under the Retirement Mortgage Programme:

- The Society’s usual lending criteria will apply

- Applicants can access our standard range of mortgage products and up to 75% LTV

- Employed applicants will be required to submit last 6 months payslips

- Self-employed applicants need to have been self-employed for at least the last 2 years prior to application

- Applicants must have good credit history and not be in adverse credit

- We will only offer a mortgage if it is in the best interests of the applicant